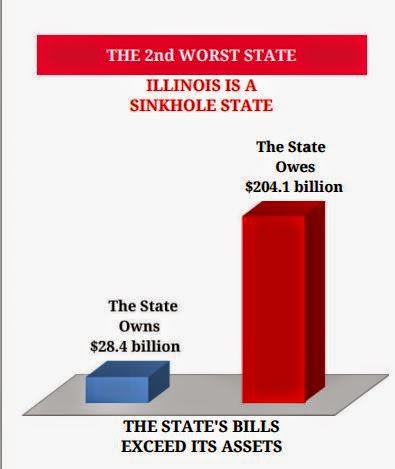

The state’s deep financial problems helped earn it that moniker. Illinois cannot pay its bills: Truth in Accounting, a nonpartisan, non-profit financial watchdog, says the state has only $28 billion dollars to pay $204 billion worth of bills, made up of state bonds, capital asset debt, underfunded pensions and healthcare benefit debts, among others.

Technically, Illinois has $73.2 billion in assets, but TIA executives say only $28.4 billion of that is available to pay bills because much of what the state has is not liquid. It’s assets are in property or land value or are restricted by law. Much what the state owes was supposed to be paid in previous years, but instead has been shifted to future budgets.

Go read the full story over at Reboot Illinois. Also, the Truth in Accounting website has a pretty handy database that allows for a state-by-state comparison of financial and demographic data across multiple categories. Here's some information about TIA in case you're wondering about who they are and what they do.

I'm sure that some rationale will be offered over the coming days as to why this data point really isn't a big deal. For example, all of the money doesn't have to be paid back at one time (although that's true of credit card debt, yet we urge against its accumulation). I would also expect that some will question the numbers. TIA does explain how they incorporate financial data into their analysis:

Why are your numbers (TIA State Analysis and The Financial State of the States) different from those I find elsewhere?

Some sources omit the cost of pension and health insurance promises made by state governments to their employees upon retirement. Others assign all responsibility for state retiree pensions to taxpayers although some funding comes from other sources such as investments. Some independent appraisals of the present value of future retirement liabilities use their own estimated interest rate to discount those liabilities, while Truth in Accounting (TIA) takes uses state discount rates applied by the state actuaries. Although other independent appraisals add obligations expected to be incurred due to growth in government workforces, TIA does not make adjustments like this. Given that they account for assets available to pay bills as well as the use of other borrowing, TIA’s estimates provide a broader perspective of each state’s financial position, including retirement liabilities.

No comments:

Post a Comment